How to Get a Refund After Being Auto-Renewed

How to get a refund after being auto-renewed: the exact email to send, the deadlines that matter, and why a chargeback can lock your account.

You opened your statement, and there it is: a charge you forgot was coming, for a year of something you used twice. The renewal already went through. Now you want your money back, and the help page is cheerfully telling you all sales are final.

Here is the short version. Email the merchant directly, fast, ideally within 24 to 48 hours, and lead with the fact that you have not used the account. That single move recovers more money than anything else, even when the policy says no refunds. Only reach for a card chargeback if the merchant refuses and you have a genuine reason, because a chargeback is slower, it can sour the relationship, and on an Apple, Google, or PlayStation purchase it can get your account locked.

The rest of this page is the playbook: the exact words to send, the deadlines that actually matter, and an honest map of when a chargeback helps you versus when it blows up in your face.

You are not an edge case, by the way. C+R Research found in 2022 that 42% of consumers had forgotten about a subscription they were still paying for, and the same survey put the gap between what people think they spend and what they actually spend at about $133 a month. The renewal that just hit you is the most ordinary financial event in the world. That is also why merchants have a quiet process for handing the money back. You just have to ask the right way.

Step 1: Ask the merchant directly, and ask fast

Before you do anything clever, send one email. Not a chargeback, not a tweet, not a threat. An email to the company that charged you.

Speed is the whole game here. A refund request that arrives the day of the charge reads as "this was clearly an accident, please fix it." The same request three weeks later reads as "I had second thoughts." Same facts, completely different odds. Send it within 24 to 48 hours if you can.

Then lead with your strongest argument, which is almost always account inactivity. If you have not logged in since the last billing cycle, say so plainly: "I have not used the service since [date]." A merchant looking at a dormant account knows the renewal was a mistake, not a decision, and giving you the money back costs them almost nothing. It is the single most persuasive line you can write.

A few things that help:

- Be polite but immovable. The person reading your email may be trained to offer you a discount, a pause, an extra month, anything except a refund. Thank them and repeat the ask. You want a refund, not a coupon.

- Name the charge precisely. The exact amount, the exact date, the plan name. It signals you are organized and not going away.

- Ask for a supervisor if the first answer is no. Frontline reps often have a hard ceiling; a supervisor can usually approve a "one-time exception." That phrase, by the way, is doing a lot of work. It is rarely one time, and it is rarely an exception.

If the merchant says yes, you are done. Most of the time, if you got there fast and the account is unused, they will.

Step 2: Refund or chargeback? Get this call right

If the merchant flat-out refuses, the temptation is to call your bank and dispute the charge. Before you do, understand what a chargeback actually is, because the internet treats it like a free backup and it is not.

A refund is the merchant handing your money back. A chargeback is you going over the merchant's head to the card network and forcing the money back, against the merchant's wishes. The second one has a blast radius.

Default to the refund path for three reasons:

- It is faster. A goodwill refund can land the same day. A chargeback is a multi-week process during which you may still be in billing limbo.

- It costs the merchant a fee, up to $100 per chargeback according to Recurly, on top of refunding you. That makes them less inclined to help, and a merchant is well within its rights to ban a customer who charges back.

- On app-store purchases, it can lock your account. More on that in Step 3.

So the real question is whether you even have a valid chargeback reason. The FTC, under the Fair Credit Billing Act, defines a billing error narrowly: charges that were unauthorized, for things you did not accept or that were not delivered as agreed, or for the wrong amount (FTC, disputing charges). Map your situation honestly:

| Your situation | Valid chargeback reason? | Why |

|---|---|---|

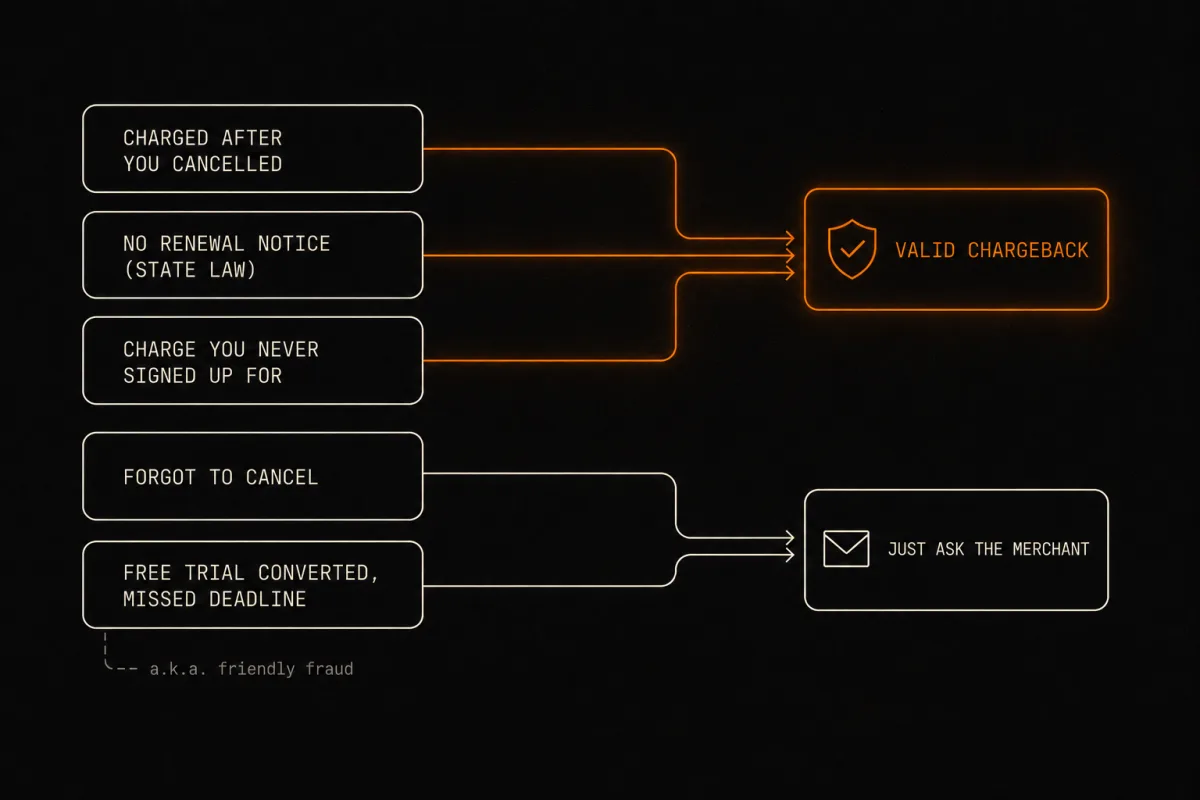

| Charged after you cancelled | Yes | Unauthorized and not as agreed. Bring your cancellation confirmation. |

| No renewal notice sent where your state requires one | Yes, often | The renewal may be unauthorized under state law (see Step 4). |

| You do not recognize the charge or never signed up | Yes | Unauthorized. |

| You forgot to cancel, but you did sign up for auto-renew | Generally no | This is buyer's remorse. Networks call it "friendly fraud." Ask the merchant instead. |

| A free trial converted and you missed the deadline | Weak | Same category. The merchant's goodwill is your real path. |

Here is the line nobody else will tell you plainly: forgetting to cancel is not, by itself, grounds for a chargeback. You agreed to auto-renew, the merchant has your consent on file, and if you dispute it the merchant can win. Card networks have a name for disputing a charge you actually authorized, and it is friendly fraud. Visa defines it as "when a cardholder disputes a legitimate transaction that they made," and in its 2025 Global eCommerce Payments and Fraud Report Visa put friendly fraud at around 20% of all fraudulent disputes globally, rising toward 30% for high-volume online merchants. A forgot-to-cancel dispute lands squarely in that bucket. That does not mean you are out of luck. It means your lever is a good email, not a chargeback. Save the chargeback for when you genuinely have one of the "yes" rows above.

Step 3: If the charge came through an app store, do NOT call your bank first

This is the part the rest of the internet skips, and it is the most expensive thing to get wrong.

If you bought the subscription through Apple, Google Play, PlayStation, or Roku, and you dispute the charge with your bank instead of the platform, the platform can disable or lock your account. To get back in, you may have to repay the exact amount you just disputed. This is a documented pattern, not a horror story. Sony freezes PlayStation Network accounts over chargebacks until the disputed amount is repaid, and riders have reported being banned from Lyft after charging back a Citibike subscription. Many terms of service treat a chargeback as a breach of your payment agreement and let the company suspend you for it. Apple steers you to its own Report a Problem refund tool precisely so the dispute never reaches your bank.

Think about what is at stake. Your Apple ID is not just one subscription. It is your purchased apps, your music, your photos in iCloud, the lot. Charging back $59 to your bank and losing access to all of it is a terrible trade.

So the order is non-negotiable for platform-billed charges:

- Use the platform's own refund tool first. On Apple it is Report a Problem. On Google Play it is the Order History refund request. These exist precisely so you do not go to your bank.

- Only if the platform refuses, and only if you have a valid reason, consider a bank dispute, knowing the account risk.

If you cannot tell which charge came from where, that is a separate and common problem. A statement line like "APL*ITUNES" or a renamed billing descriptor hides what you actually subscribed to. Our guide on why a subscription shows a different name on your statement walks through decoding those, and if the charge is genuinely a mystery, start with a recurring charge you don't recognize instead of assuming it is yours.

Step 4: The rights lever most people never use

Here is how to turn a weak "I forgot" into a strong "you broke the law." In several states, a company has to warn you before an auto-renewal charge. If it did not send that warning, the renewal itself may be unauthorized, which can make the whole charge refundable.

California has the Automatic Renewal Law. For a subscription with an initial term of a year or longer, the business must send a renewal notice 15 to 45 days before renewing, spelling out the terms, the amount, the frequency, and how to cancel (California Business and Professions Code Section 17602). The teeth are real: when a business violates the ARL, California treats whatever it provided under that unauthorized subscription as an "unconditional gift," meaning you can keep it and may be owed a refund of what was charged.

New York has General Business Law Section 527-a. For an auto-renewal with an initial paid term of a year or longer, the business must notify you between 15 and 45 days before the cancellation deadline, through your chosen channel, with instructions on how to cancel.

Colorado, Illinois, Connecticut, and Vermont have their own auto-renewal notice laws too, and the list keeps growing. At the federal level, the Restore Online Shoppers' Confidence Act (ROSCA) is still live law. It requires clear disclosure of auto-renewal terms, your informed consent before charging, and a simple way to cancel.

One honest correction, because a lot of articles still get this wrong: the FTC's "click-to-cancel" rule is not in force. It was vacated by the Eighth Circuit on July 8, 2025, days before its compliance date, on a procedural defect. The FTC has restarted that rulemaking, and ROSCA enforcement continues, but do not let anyone tell you click-to-cancel is the law you can cite today. ROSCA and your state's ARL are the levers that actually work.

To use the lever, put one sentence in your email:

"I never received the renewal notice that [California / New York] law requires before an auto-renewal charge. Because that notice was not sent, this renewal was not properly authorized, and I am requesting a full refund."

That converts a favor you are asking for into a right you are claiming. The tone change does a lot. For the bigger picture on which rules are live, which are dead, and who is enforcing what, see our FTC subscription crackdown scoreboard.

The copy-paste email

Here is the whole thing in one block. Adapt the brackets and send it.

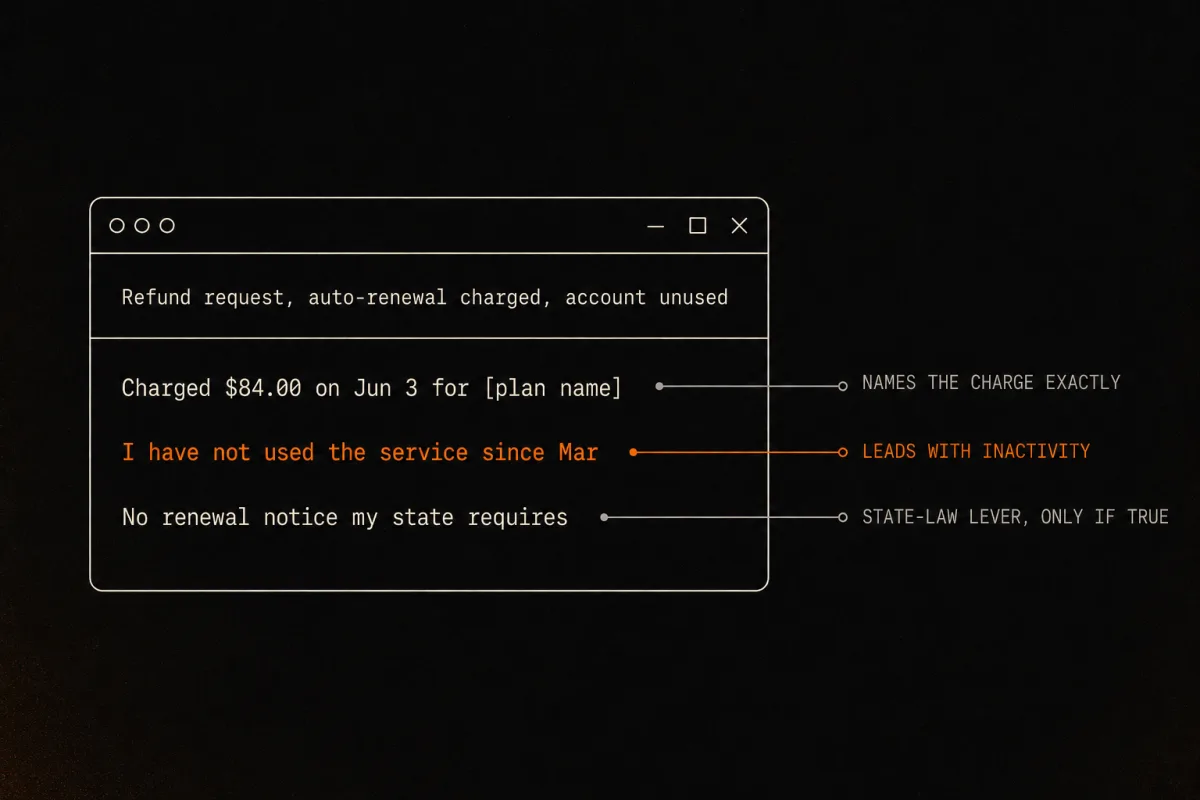

Subject: Refund request, auto-renewal charged [date], account unused

Hi,

I was charged [$amount] on [date] for the auto-renewal of [plan name] on the account under [email / account ID].

I have not used the service since [date or last login], and I no longer want the subscription. I would like to cancel it and request a full refund of this renewal.

[If applicable: I also did not receive the renewal notice that [state] law requires before an auto-renewal charge, so this renewal was not properly authorized.]

I would much prefer to resolve this with you directly. Thank you for your help.

[Your name]

Notice what that email does and does not do. It leads with inactivity. It names the charge exactly. It mentions the state-law lever only if it is true. And it says "resolve this directly," which is a quiet way of letting them know a dispute is possible without opening with a threat. You are giving them an easy yes. Most of the time, they take it.

If the first reply is a discount offer, reply once: "Thank you, but I am requesting a refund and cancellation, not a discount." If the second reply is still no, ask for a supervisor. If the supervisor says no and you have a valid reason from the Step 2 table, then, and only then, you escalate to a dispute.

When the stonewalling is the point

Sometimes you will do everything right and still hit a wall: no refund button, a support email that bounces you through three bots, a "cancel" link that leads to a retention maze. That is not your failure. It is a design choice. Companies that make refunds and cancellations hard are betting you will give up, and most people do.

Disputed and failed payments are not a rounding error for these businesses either. Recurly projected that involuntary churn, the failed and disputed payments side of the ledger, could cost subscription companies more than $129 billion in 2025 in the US alone. That is the industry's loss, not your gain, but it tells you something useful: the money moving back and forth on disputed subscriptions is enormous and routine. You asking for one refund is a Tuesday. If you want to understand why the cancel and refund flows are engineered to exhaust you, we wrote about why companies make you call to cancel.

Frequently asked questions

Can I get a refund for a subscription I forgot to cancel? Often yes. Ask the merchant fast, ideally within 24 to 48 hours, and lead with the fact that the account shows no usage. Plenty of companies grant a goodwill refund even when the policy says no refunds. Forgetting is not grounds for a card chargeback, but it is a perfectly good reason to send a polite, well-argued refund request.

Is it better to ask for a refund or do a chargeback? Ask for a refund first. It is faster and it does not put a dispute on your account. A chargeback should only come later, if the merchant refuses and you have a valid reason: you were charged after you cancelled, you never got a renewal notice your state requires, or you did not authorize the charge at all.

What if I was charged after I already cancelled? That is an unauthorized charge, which the Fair Credit Billing Act treats as a billing error. Find your cancellation confirmation (email, screenshot, or a saved chat) and send it with your request. This is one of the clearest valid disputes you can have.

Can a chargeback get my Apple or Google account banned? Yes. If you bought through Apple, Google Play, PlayStation, or Roku and you dispute the charge with your bank instead of the platform, the platform can lock or disable your account, and you may have to repay the disputed amount to get back in. Use the platform's own Report a Problem refund tool first.

How long do I have to dispute a subscription charge? With your card company, the Fair Credit Billing Act gives you 60 days from the date the first statement showing the charge was sent. Card-network chargeback windows are often longer, commonly up to 120 days, but sooner is always stronger. Ask the merchant directly within a day or two of the charge for the best odds.

The company never told me it was renewing. Do I have rights? Maybe. In California, New York, and a growing list of states, a business has to send a renewal notice in a set window before charging you. If it did not, the renewal may be unauthorized under that state's law, which can make the whole charge refundable.

What is the strongest argument for a refund? Account inactivity. Zero usage during the period you got charged for is the most persuasive line you can put in the email. It tells the merchant the renewal was an accident, not a decision, and it costs them little to make it right.

Get ahead of the next renewal instead of chasing it

Refunds are the cleanup. The better outcome is seeing the renewal before it lands, while cancelling is still a calm decision instead of a scramble for your money back.

That is what Subcut does. It reads your bank statement, surfaces every recurring charge, and shows you the renewals coming up, so you can decide ahead of time rather than in the cancel flow. It will not message the merchant for you or auto-refund anything; the human still does the asking. Most people who end up chasing a refund had seen the charge before, somewhere. Seeing it is not enough. Acting on it is. One honest note: the statement import sends your file to a remote service to read it, so it is not fully on-device. We would rather tell you that than pretend otherwise.

So you find the next forgotten renewal, the kind that hides inside the roughly $133 a month people underestimate their spending by, before it auto-renews, not after.

iOS - Free to use - No subscription required (ironic, we know)

Keep going

Sources

- FTC: Using Credit Cards and Disputing Charges

- C+R Research 2022 subscription survey, via CNBC

- Visa: Friendly fraud (2025 Global eCommerce Payments and Fraud Report)

- Recurly: chargebacks and subscription billing (up to $100 per chargeback)

- Recurly: failed payments could cost subscription companies more than $129 billion in 2025

- California Business and Professions Code Section 17602 (Automatic Renewal Law)

- New York General Business Law Section 527-a

- Gibson Dunn: FTC restarts negative-option rulemaking after Eighth Circuit vacatur