Subscription Cost Calculator: What You Really Spend

A subscription cost calculator that adds up your monthly, yearly, and 10-year spend, then compares it to sourced US averages. Honest math, no number-vomit.

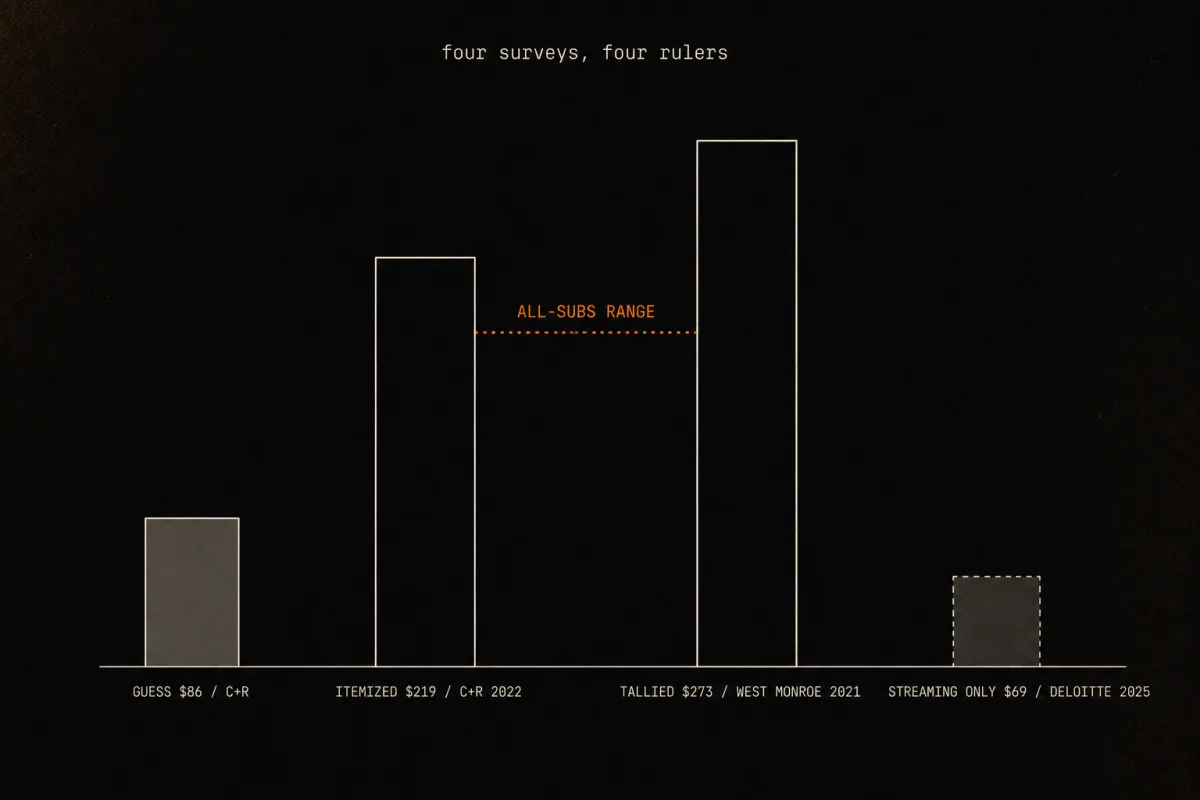

You have a rough number in your head for what your subscriptions cost. It is almost certainly too low. When C+R Research asked people to guess their monthly subscription spend in 2022, the average guess was $86. When the same people sat down and itemized it, the real figure was $219 a month, about two and a half times the guess (C+R Research, 2022).

So here is the direct answer to "what do I really spend on subscriptions": add every recurring charge to get a monthly total, multiply by 12 for a yearly floor, and treat that as a minimum because prices keep rising. The calculator below does it for you, then shows the 5-year and 10-year totals most people never look at. The honest part comes after the math.

The calculator

Add each subscription with its price and billing cycle. The total updates as you go.

Nothing added yet. Pull up a statement and list each recurring charge.

Prefer not to type? Import a bank or card statement and let Subcut find the recurring charges for you. One honest note on that, because we would rather you hear it from us: statement import uploads your file to a remote service that reads it. It is not processed only on your phone. If that matters to you, the manual calculator above never sends anything anywhere.

What the "average" actually is (and why nobody agrees)

Most subscription calculators slap a confident "the average American spends $200+ a month" under the widget with no source attached. We are not going to do that, because the honest answer is more interesting: the published averages genuinely disagree, and the disagreement tells you something useful.

Here is the same question, answered by four credible sources, each measuring a slightly different thing:

| Source (year) | What it measured | The number |

|---|---|---|

| People's own guess (C+R Research, 2022) | Offhand estimate before itemizing | ~$86/month |

| C+R Research, 2022 | All subscriptions, itemized | ~$219/month |

| West Monroe, 2021 | All subscriptions, tallied across 21 categories | ~$273/month |

| Deloitte, 2025 | Video streaming only | ~$69/month |

Read that table once and you can see why "the average" is a trap.

The $86 figure is a guess, not measured spend. Both C+R and West Monroe found the same thing: people lowball it badly. West Monroe's 2021 poll of 2,500 US consumers found that 100% of respondents underestimated their actual spend, and 66% were off by more than $200 (West Monroe, 2021). The first 10-second guess in that study averaged $62 a month; given another 20 seconds to think, people revised up to $96 (West Monroe via PR Newswire, 2021). The harder they thought, the higher it climbed, and they still landed short.

The $219 versus $273 gap is not a contradiction. It is mostly about what counts. West Monroe forced respondents to tally across 21 categories (streaming, music, software, gym, meal kits, news, cloud storage, gaming, subscription boxes, and more), which surfaces more spending than a shorter list. C+R's itemized approach landed lower. Both are honest "all subscriptions" numbers; they just cast different-sized nets.

The $69 figure is the one to watch for. It is Deloitte's 2025 average for video streaming only, and it held flat year over year. It is not comparable to the all-subscription figures, and several competitor calculators quietly conflate the two. Streaming is a slice of your subscriptions, not the whole pie.

So what is the real current average? We are not going to invent one. The surveys span 2021, 2022, and 2025, prices have risen since, and there is no clean recent primary source for an all-subscription US figure. The honest framing is a dated range: somewhere around $219 (C+R, 2022) to $273 (West Monroe, 2021) a month for all subscriptions, with people themselves guessing about $86. The average is a moving target. That is precisely why measuring your own number, which the calculator above does, beats trusting a benchmark.

Why your total is bigger than it feels

The gap between what people think they spend and what they actually spend is not a math error. It is the design working as intended. Two forces keep your real number invisible:

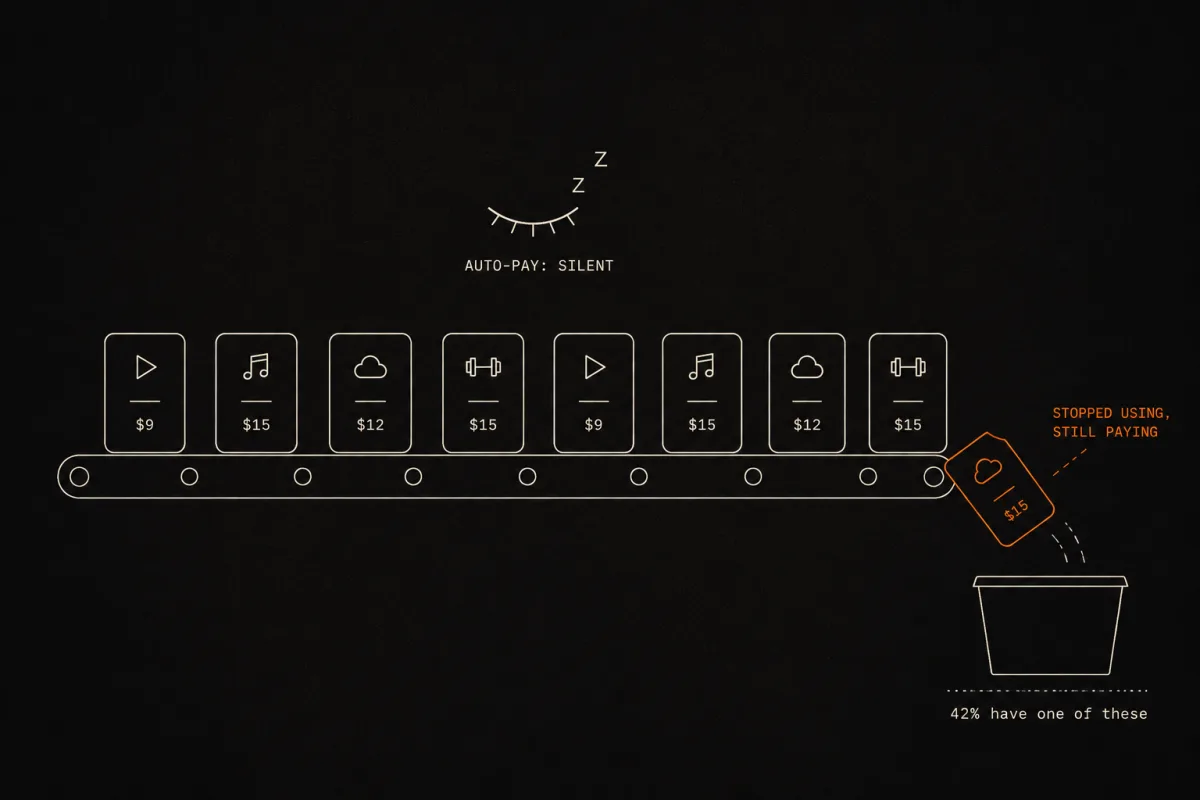

Auto-pay makes the charges silent. In C+R's 2022 survey, 72% of people had set their subscriptions to auto-pay, and 74% said it was easy to forget about recurring monthly charges (C+R Research, 2022). A charge you never see is a charge you never question.

Forgetting is the norm, not the exception. A 2021 Chase survey of more than 2,000 Americans found that 60% had forgotten about at least one recurring payment, and 55% did not know how much was leaving their account each month in recurring charges (Chase, 2021). C+R's number is the kicker: 42% admitted they had stopped using a subscription but kept paying for it anyway (C+R Research, 2022).

That last one is the money line. Almost half of people are paying, right now, for something they decided to stop using and never finished cancelling. A calculator that adds up your real charges is mostly a tool for finding those.

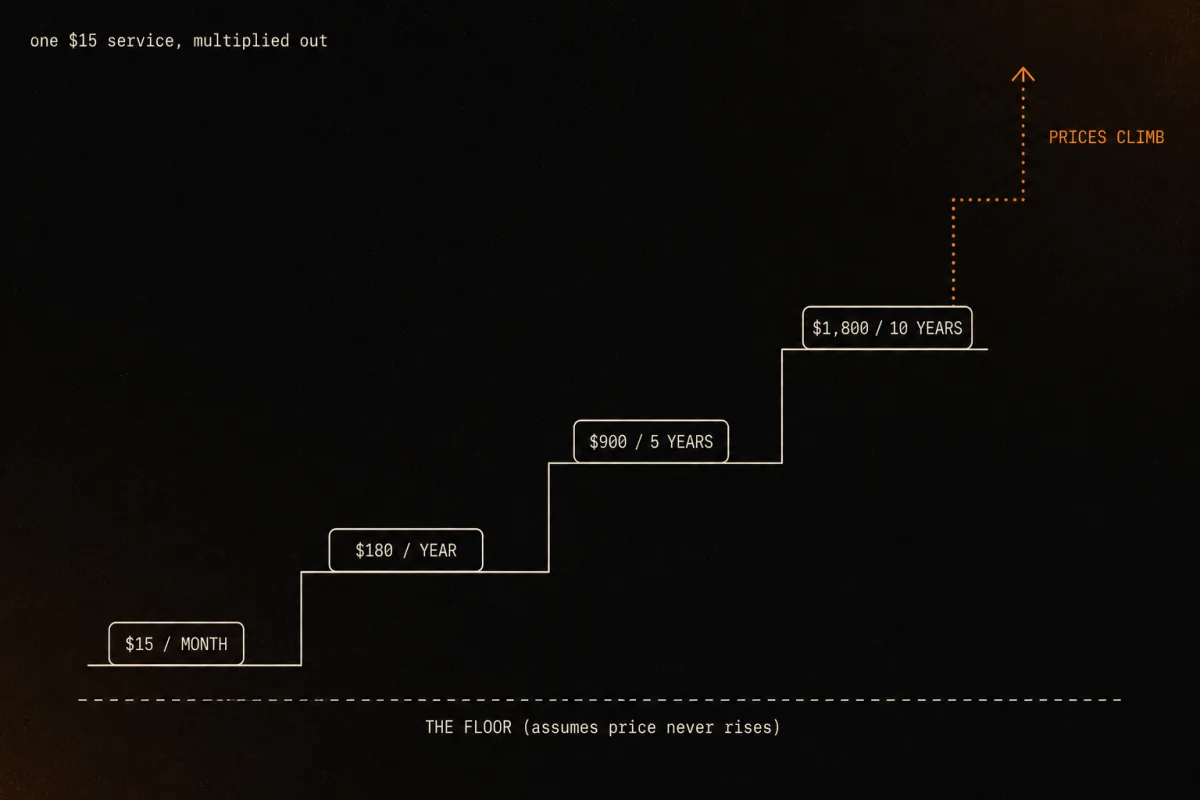

The long-horizon number nobody multiplies out

A $15 streaming service feels like nothing. Here is the part the monthly price hides: $15 a month is $180 a year, $900 over five years, and $1,800 over ten. And that is the floor, because it assumes the price never goes up, which it will. Deloitte found 73% of streaming subscribers are already frustrated that their services keep raising prices (Deloitte, 2025).

The calculator shows your 5-year and 10-year totals for exactly this reason. A straight monthly-times-120 is the optimistic version. Reality runs higher.

An illustration, not a forecast: opportunity cost

Here is a way to feel the long-horizon number, with every caveat attached because this is where calculators usually start lying to you.

The S&P 500 has returned about 10% a year on average over the long run, including dividends (Fidelity). So you will see breathless calculators claim that a $40-a-month subscription "really" costs you thousands in forgone investment growth. The reframe is fair: the true cost of a subscription is the price plus whatever those dollars could have done elsewhere. But the honest version comes with three asterisks competitors skip:

- It is an illustration, not a promise. Past returns do not predict future returns, and Subcut is a tracker, not an investment product. We are not going to make you this money.

- After inflation, the real return is closer to 6.5%, not 10%, so the nominal figure overstates actual purchasing power (SmartAsset).

- Individual years swing hard, with sharp gains and steep losses. The 10% is a multi-decade average, not something any single year owes you.

With those attached, the reframe still holds: a subscription you do not use is not "cheap," it is the price tag plus the growth those dollars never got to have. That is worth feeling. It is not worth lying about.

What Subcut actually sees on real statements

Every average on this page is a borrowed survey number from 2021, 2022, or 2025. Here is the one thing a survey cannot give you and a competitor calculator cannot publish: what shows up on real statements right now.

When people import a statement into Subcut, what comes back is the actual list of recurring charges on that card, with a real monthly total attached. That is not a guess and it is not a 2022 poll. It is what the recurring charges on actual cards look like, which is the closest thing to a current answer anyone has.

The pattern underneath all of it is consistent: people guess around $86, surveys measure $219 to $273, and a real statement usually lands somewhere that surprises the person looking at it. The number in your head is the least reliable one. The number on your statement is the truth.

After the total: can you even cancel easily?

The payoff of any subscription calculator is the same: now go cancel the ones you do not use. Fair question to ask before you start: is cancelling actually easy now?

For a brief moment it looked like it would be. The FTC's revised Negative Option Rule, often called "click-to-cancel," would have required cancellation to be as simple as signing up. Then a three-judge panel of the Eighth Circuit Court of Appeals vacated the entire rule on July 8, 2025, on procedural grounds, days before it would have taken effect (Cooley, 2025).

So for now it is still on you. The good news is that the older federal backstop, the Restore Online Shoppers' Confidence Act (ROSCA), is still in force and still requires a simple way to stop recurring charges, and several states (California, Colorado, New York, Connecticut, Vermont, Illinois) have their own auto-renewal and easy-cancel laws. Even after the vacatur, federal and state regulators are likely to keep enforcing those (WilmerHale, 2025). Cancelling is supposed to be getting easier. The rule that would have forced it got struck down, so the work of finding the charges is, for the moment, yours.

If you do find a charge that already renewed and you want your money back, our walkthrough on how to get a refund after an auto-renewal covers what actually works.

How to use the calculator well

- Pull up your statement first. Memory is the unreliable input here, and the surveys prove it. Work from the actual list of charges, not the one in your head. The fastest way is to import a statement and let the recurring charges get found for you.

- Convert everything to the same cycle. A weekly $4 charge is about $17 a month, not $4. The calculator handles the conversion so a $99-a-year plan and a $9-a-month plan sit side by side honestly.

- Read the 10-year total out loud. That is the number that changes behavior. The monthly price was designed to be forgettable. The decade total is not.

- Flag the ones you forgot you had. Those are your easiest wins, and per C+R's 42%, you almost certainly have at least one.

- Decide monthly versus annual on purpose. Annual is cheaper per month only if you keep the service past the break-even point (annual price divided by monthly price). Below that month, you overpaid for flexibility you did not use.

Frequently asked questions

How much does the average person spend on subscriptions per month? It depends on the survey and what counts as a subscription. For all subscriptions combined, C+R Research put it at about $219 a month in 2022, and West Monroe put it at about $273 a month in 2021. For video streaming only, Deloitte found about $69 a month in 2025. People themselves guess around $86. There is no single current "average," which is exactly why measuring your own number beats trusting a benchmark.

Why is my actual subscription spend so much higher than I thought? Because almost everyone guesses low. C+R Research found people estimated $86 a month but actually spent about $219 once they itemized. West Monroe found 100% of respondents underestimated their spend. Auto-pay and forgetting do the rest: Chase found 60% of people have forgotten about at least one recurring payment.

How do I calculate the true annual cost of my subscriptions? Add up every recurring charge to get your monthly total, then multiply by 12 for a yearly floor. Treat that as a minimum, not the final number: prices rise over time, so a straight monthly times 60 or times 120 understates your real 5-year and 10-year cost. The calculator on this page does the multiplication and flags that prices climb.

What's the difference between monthly and yearly subscription pricing, and which is cheaper? Annual plans usually cost less per month, but only pay off if you keep the service past the break-even month. Divide the annual price by the monthly price to find that month. Cancel before it and monthly would have been cheaper. After it, annual wins.

How can I see all my subscriptions in one place? Add them by hand in the calculator above, or import a bank or card statement so the recurring charges get found for you. To be clear about how that works: statement import uploads your file to a remote service that reads it, so it is not processed only on your phone.

Is the FTC "click-to-cancel" rule still in effect? No. The Eighth Circuit Court of Appeals vacated the FTC's revised Negative Option Rule on July 8, 2025, days before it would have taken effect. The older federal law (ROSCA) and several state auto-renewal laws still apply, but the rule that would have forced cancellation to be as easy as signup is not in force.

How much could I save by cancelling unused subscriptions? Chase found 71% of people believe they waste more than $50 a month on recurring charges they do not need. Your real number is whatever the calculator shows for the services you no longer use. The opportunity-cost illustration on this page shows what those dollars might have grown to if invested instead, labeled as an illustration, not a promise.

See the total, then keep it from creeping back

A calculator gives you one honest snapshot. The problem is that subscriptions do not hold still: a free trial converts, a price quietly goes up, a new service sneaks on next month. Subcut watches the recurring charges on your card so the next surprise renewal is something you decide on ahead of time, not something you discover three statements later. If you want an ongoing tracker rather than a one-time tally, here is how Subcut compares to a paid tool like Rocket Money.

iOS · Free to use · No subscription required (ironic, we know).

Researched and written by the Subcut team. Last verified: 2026-06-17.

Spot something off, like a number that has moved or a source that changed? Tell us and we will re-verify.

Keep going

Sources

- C+R Research, Subscription Service Statistics and Costs (2022)

- CNBC, Consumers spend $133 more monthly on subscriptions than they realize (2022)

- West Monroe, Americans are spending more on subscriptions and are less aware (2021)

- Deloitte, Digital Media Trends survey (2025)

- Chase, Survey on recurring payments (2021)

- Fidelity, The average stock market return (S&P 500 ~10% nominal)

- SmartAsset, S&P 500 average annual return (~6.5% real after inflation)

- Cooley, Eighth Circuit vacates the FTC's Negative Option Rule (2025)

- WilmerHale, Eighth Circuit vacates the click-to-cancel rule; regulators likely to remain active (2025)