A Recurring Charge You Don't Recognize: What to Do

A recurring charge on your bank statement you don't recognize is usually a forgotten subscription, not fraud. How to identify it, then cancel or dispute in the right order.

There it is on your statement: a charge you have no memory of agreeing to, recurring every month, for an amount that does not ring a bell. Your stomach drops a little. The first word that comes to mind is fraud.

Here is the calm version, and it is true most of the time. A recurring charge you don't recognize is usually a subscription you actually signed up for and forgot about, billing under a payment processor or parent-company name you don't recognize. So the first move is not to call the bank and not to dispute it. The first move is to identify it. Then, if you want it gone, cancel the source, ask for a refund, and only dispute as a last resort. Do those steps out of order and you can get your own dispute denied.

The rest of this page is the method: how to tell which of three things you are looking at, the exact next step for each, and the deadline math that decides how fast you have to move (it is different for credit and debit, and almost nobody tells you that).

First, the odds: it's probably not fraud

The whole internet leads with "it might be fraud!" because fear gets clicks. The honest framing is calmer and more useful. The most likely explanation for a recurring charge you can't place is a forgotten subscription, not a thief.

C+R Research found in 2022 that 42% of consumers had kept paying for a subscription they had forgotten about, and the same survey put the gap between what people think they spend on subscriptions and what they actually spend at about $133 a month ($86 estimated versus $219 itemized). You are not careless. You are one of almost half of all subscribers, and the charge that just spooked you is the most ordinary financial event there is.

Leading with the odds is not about making you complacent. It is to keep you from the panicked move (a bank dispute) before the smart one (identifying it), because the panic move can actually cost you the refund.

Step 1: Identify the charge before you act

Every branch starts the same way. A charge you cannot name is a charge you cannot cancel and should not dispute yet. Spend five minutes here first.

- Read the exact descriptor. Note the full text, including any prefix or asterisk (like

PADDLE.NET*orSQ *), the amount to the cent, the date, and the cadence (monthly, annual, or something odd). - Search the exact descriptor string and the amount in your email inbox and on the web. A receipt or a confirmation email is the fastest way to recognize your own charge. The exact dollar amount is often a better search term than the name.

- Check who else is on the card. A partner, a kid, an authorized user. A surprising share of "mystery" charges are someone you live with, which the chargeback industry politely calls friendly fraud that is a family affair.

- Check the platform purchase histories where subscriptions hide: Apple's reportaproblem.apple.com, Google Play order history, Amazon memberships, and PayPal activity.

One tip that resolves a lot of Apple cases: an iCloud+ storage charge does not show up under Settings > Subscriptions. It lives under Settings > [your name] > iCloud > Manage Storage. People hunt the Subscriptions screen, find nothing, and assume fraud, when the charge was hiding one menu over the whole time.

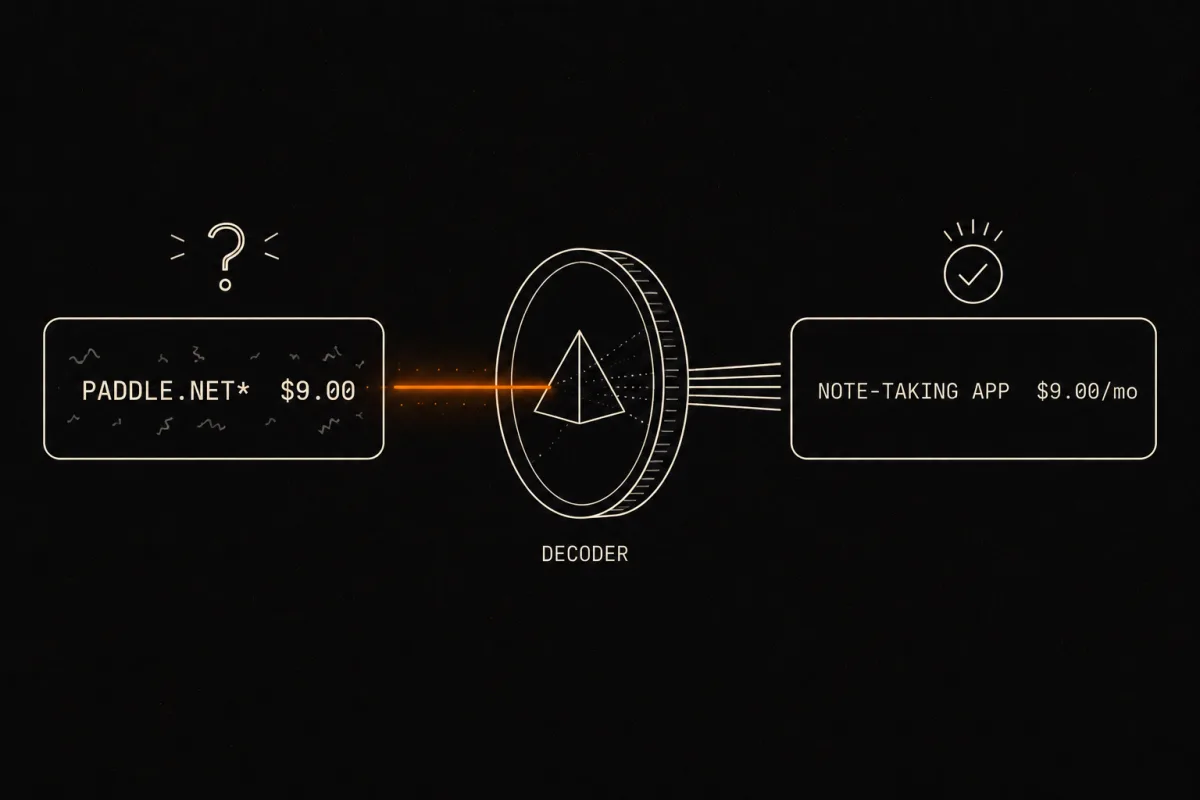

If you do all that and the name is simply wrong (the charge is clearly legitimate but it is not the brand you know), that is its own well-trodden problem. We wrote a full decoder for it: why a subscription shows a different name on your statement.

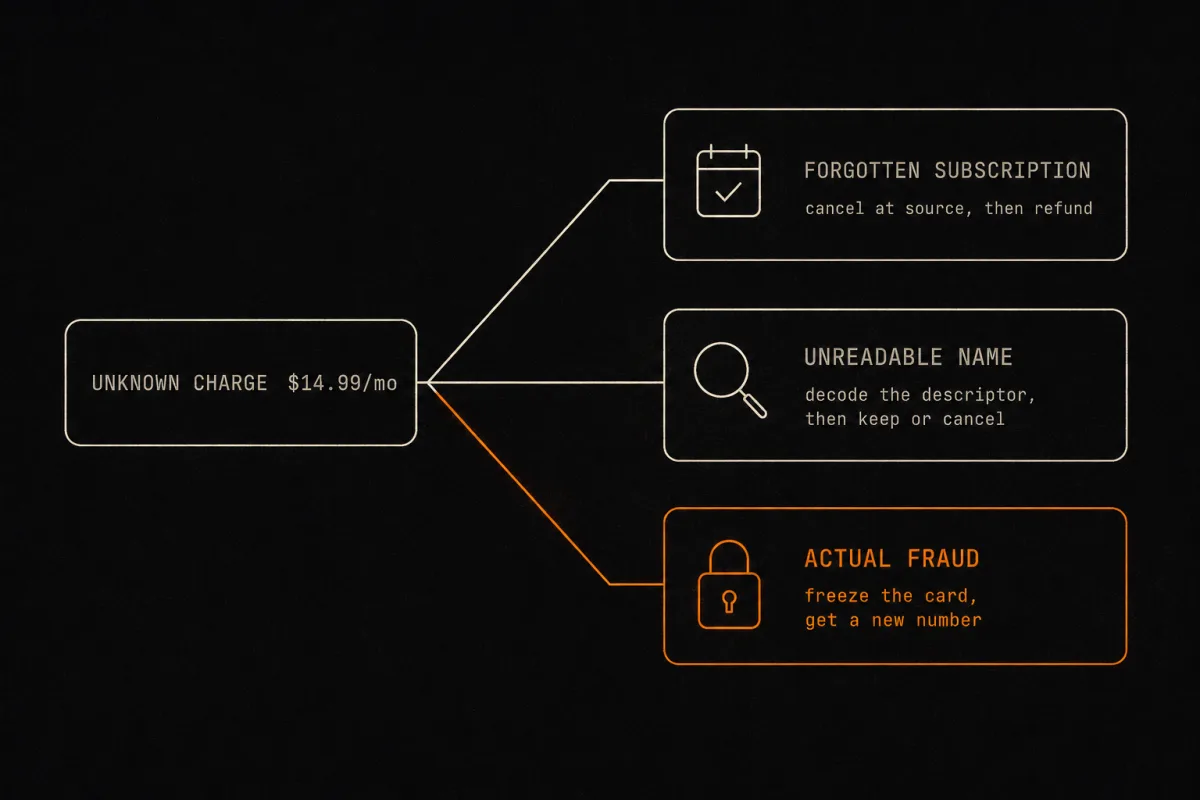

Step 2: Figure out which of three things you're looking at

Almost every unrecognized recurring charge is one of three things. The triage is the whole point, because the right action is different for each.

| Branch | The tell | First action |

|---|---|---|

| 1. Forgotten subscription (most common) | Amount matches a known service price, recurs on a clean monthly or annual cadence, a receipt exists in your email, it traces to a real account you own | Cancel at the source first, then ask for a refund |

| 2. A real merchant you don't recognize | The charge is legit but the name is a processor, parent company, or truncated legal name (PADDLE.NET, FSPRG, SQ*, APPLE.COM/BILL, AMZN) | Decode the name back to the app, then treat it as Branch 1 |

| 3. Actual fraud | No account, no receipt, no family member, undecodable after Step 1, or tiny clustered "test" charges, or charges after you cancelled | Freeze the card now, get a new number, dispute within the legal window |

Branch 2 is the one people most often misfile as fraud and wrongly dispute. The charge is yours, you just could not read the name. The usual culprits are payment processors and parent companies: a PADDLE.NET, an FSPRG, an APPLE.COM/BILL, a truncated legal name. If that is you, the different-name decoder walks the whole processor map. Once you have a name, a Branch 2 charge becomes a Branch 1 charge: keep it and do nothing, or cancel it at the source.

Step 3: The order of operations nobody else explains

This is the part that gets skipped, and it is the part that matters most. If you have decided you want the charge gone, the order is not negotiable:

- Identify the source. (You did that above.)

- Cancel the subscription at the source first. Get written confirmation.

- Ask the merchant for a refund. Politely, quickly, leading with the fact that you have not used the account. Our refund-after-auto-renewal playbook has the exact email to send.

- Dispute last, only if the merchant refuses and you have a genuine reason.

Reverse that order and you can sink your own case. This is not a Subcut opinion, it is how the card networks work.

Card networks expect you to try the merchant before you dispute. And "I forgot to cancel" is not a valid dispute reason: the industry classifies it as friendly fraud, which ChargebackGurus calls the leading cause of subscription chargebacks. Worse, if you dispute while the subscription is still live, you have not cancelled the recurring authorization, so the merchant just charges you again next month. And when the merchant pushes back, the fact that you never tried to cancel first is the evidence that wins it for them. You end up still subscribed, with a denied dispute on your account.

One more landmine. If the charge came through Apple, Google Play, PlayStation, or Roku, do not open with a bank dispute. Disputing an app-store purchase with the bank instead of the platform can get the account locked or disabled. Use the platform's own Report a Problem tool first.

When a dispute actually is valid

To be clear: plenty of unrecognized charges should be disputed. The Fair Credit Billing Act treats as billing errors any charge that is unauthorized, for something you did not accept or that was not delivered as agreed, or for the wrong amount (FTC, billing-error rules). Here is the honest map.

| Your situation | Valid dispute? | Why |

|---|---|---|

| Charged after you cancelled | Yes | Unauthorized, not as agreed. Bring your cancellation confirmation. |

| You never signed up and genuinely don't recognize it after Step 1 | Yes | Unauthorized charge. |

| Card-testing micro-charges you didn't make | Yes | Fraud. Freeze the card and get a new number first. |

| You forgot to cancel a sub you did sign up for | Generally no | Friendly fraud. Cancel and ask the merchant instead. |

| Free trial converted and you missed the deadline | Weak | Same. Merchant goodwill is the real path. |

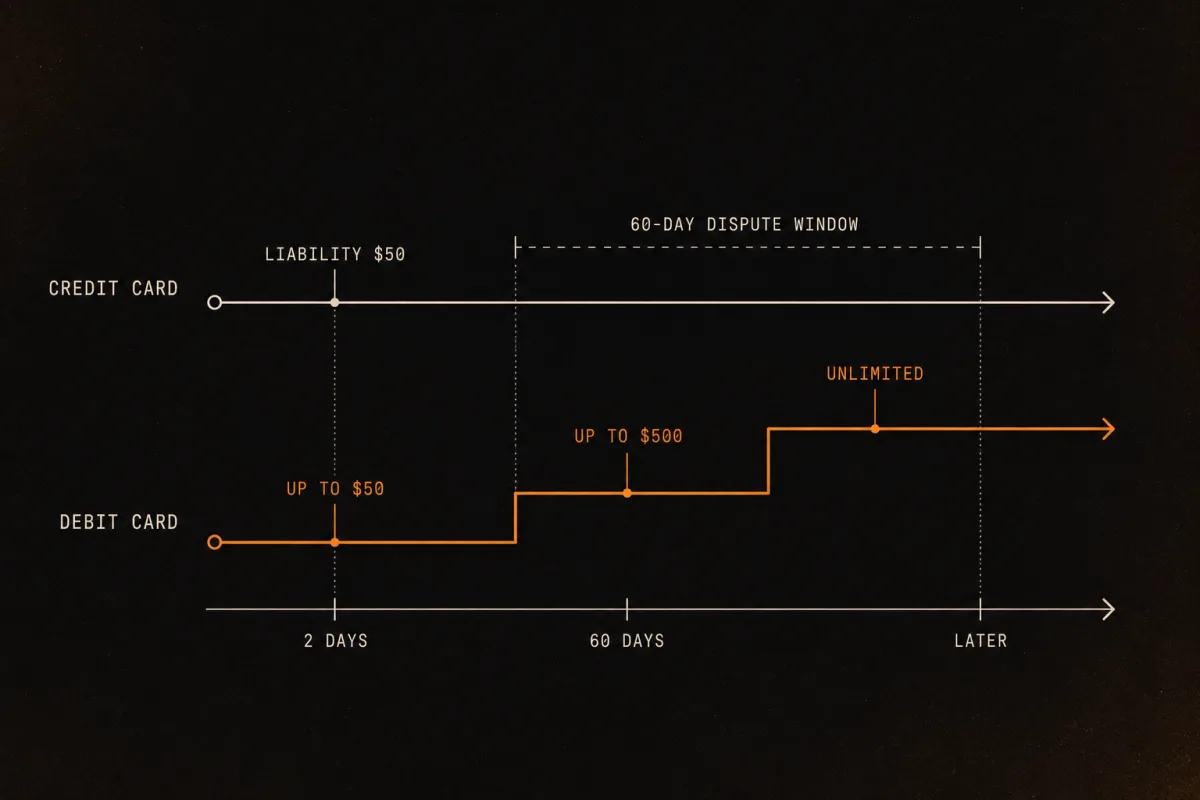

Step 4: Know your deadline (it's different for credit and debit)

If you do reach the dispute stage, the clock and your liability depend on which card got hit. This is a real, checkable difference that changes how fast you should move, and most competing guides skip it entirely.

Credit card (Fair Credit Billing Act). You have 60 days from the date the first statement showing the charge was sent to dispute a billing error in writing. Your liability for unauthorized charges is capped at $50 (and most issuers make it $0 in practice). Your issuer must acknowledge the dispute within 30 days and resolve it within two billing cycles, up to 90 days. Send the dispute to the billing-inquiries address, not the payment address (FTC, disputing credit card charges).

Debit card (Electronic Fund Transfer Act, Regulation E). The ladder is harsher, because the money already left your account:

- Report within 2 business days and your liability is capped at $50.

- Report after 2 days but within 60 days of the statement, and it climbs to $500.

- Report after 60 days, and it can be unlimited (CFPB Regulation E §1005.6).

Translation: if the mystery charge hit a debit card, treat it as the urgent case. Same charge, very different downside.

The small charge you can't identify: two different problems

The "tiny recurring charge I can't place" search hides two completely different situations, and the right move depends on the amount. Do not blur them.

A sub-$1 charge, often clustered ($0.99, $1.00, random cents). This is frequently card testing: a fraudster runs a tiny purchase to confirm a stolen card number is live before attempting a big hit. The $0.99 line is an early breach signal, and the advice is to freeze first. Lock the card in your banking app right now, then call the bank and get a new number. Do not waste time searching the merchant name. This is Branch 3.

A deliberately low recurring fee, usually under $20. This is the classic free-trial continuity play. The Minnesota Attorney General describes the negative-option trap where your silence or failure to cancel is read as permission to keep charging, and companies keep the monthly fee low on purpose so it slides under your radar. This is Branch 1. Identify it, cancel at the source, ask for a refund.

Same instinct ("it's only a few dollars, who cares"), opposite correct response. Tiny and clustered means freeze. Small but clean and monthly means cancel.

The arc to short-circuit

If you have read forums on this, you have seen the same story over and over: unfamiliar name, mild panic, assume fraud, almost file a dispute, then discover it was a real, forgotten, or just oddly-named subscription you signed up for yourself. The Apple Community mystery-subscription threads are full of it, and the resolution is almost always a subscription buried in Settings, not a thief. The method on this page exists to cut that arc off before the "almost file a dispute" step, because that step is where people lock their accounts or get a dispute denied. Identify first.

You found one. There are probably more.

A mystery charge rarely travels alone. People who go looking for one forgotten subscription usually find three, because nobody is tracking all of them and they pile up quietly under names you cannot read.

That cryptic descriptor, the PADDLE.NET* or the truncated parent company, is exactly the problem Subcut's importer was built for. You hand it your statement, it reads the whole thing and matches cryptic bank lines back to the actual app, so "I don't recognize this" turns into "oh, that's what that is" for every recurring charge at once. Being straight about how it works: when Subcut decodes a statement, the file goes to our import worker (Google Gemini, with Claude as a fallback), not to some on-device-only magic. The decoding happens on a remote worker, and we would rather tell you that than pretend otherwise. Subcut surfaces and names the charges. You decide what to cancel; it does not auto-cancel, auto-refund, or call your bank for you.

Prefer to start without an import? You can also find subscriptions from a bank statement without a bank login. And when you hit a company that makes cancelling deliberately hard, here is why they make you call to cancel, and how to win.

iOS · Free to use · No subscription required (ironic, we know).

FAQ

Is an unrecognized recurring charge usually fraud? Usually no. The most common cause is a forgotten subscription you signed up for, often billing under a payment processor or parent-company name you don't recognize. C+R Research found in 2022 that 42% of people had kept paying for a subscription they had forgotten about. Identify the charge before you assume it is fraud.

Should I cancel the subscription or dispute the charge first? Identify and cancel the source first, then ask the merchant for a refund, and only dispute if they refuse and you have a valid reason. Disputing while the subscription is still active can get the dispute denied, because "I forgot to cancel" counts as friendly fraud, not a valid billing error, and the merchant just re-bills you.

How long do I have to dispute a charge I don't recognize? On a credit card, 60 days from the date the first statement showing the charge was sent, under the Fair Credit Billing Act. On a debit card, report within 2 business days to cap your liability at $50. After that it climbs to $500, and after 60 days it can be unlimited, under Regulation E. Debit cards mean you have to move faster.

There's a tiny charge I can't identify, like $0.99. What is it? A small, odd-amount charge, especially several clustered together, is often card testing: someone checking whether a stolen card number is live before they attempt a bigger charge. Freeze or lock the card in your banking app first, then call your bank and ask for a new number. Do not just search the merchant name.

Why doesn't the charge show the name of the app I paid for? Many apps bill under a payment processor like PADDLE.NET or FastSpring, a parent company like APPLE.COM/BILL or AMZN, or a truncated legal name. The charge is real. The name is just not the brand you recognize. Decode the descriptor back to the app before you treat it as fraud.

I was charged after I cancelled. Can I dispute that? Yes. A charge after a confirmed cancellation is unauthorized and not as agreed, which is a valid billing error under the Fair Credit Billing Act. Bring your cancellation confirmation, like the email or a screenshot, when you file the dispute.

Can disputing an Apple or Google charge cause problems? Yes. Disputing an app-store purchase with your bank instead of the platform can lock or disable the account. Use the platform's own Report a Problem refund tool first, then dispute with the bank only if that fails.

Keep going

Sources

- FTC: Using Credit Cards and Disputing Charges

- FTC: Disputing Credit Card Charges (billing-error rules)

- CFPB Regulation E §1005.6 (debit-card liability)

- C+R Research 2022 subscription survey, via CNBC

- ChargebackGurus: what causes subscription chargebacks (friendly fraud)

- Minnesota Attorney General: free-trial offers with strings attached